Liam Stewart

Liam Stewart

Surging Demand for Offshore Construction Vessels: Market Outlook 2026–2028

Energy Maritime Associates (EMA) presented at the OSJ Subsea Conference in London on 2 February 2026. Our Executive Director, Michael Watson, spoke...

The Q4 2025 results from Saipem, TechnipFMC (TFMC) and Subsea7 (S7) point to an offshore services market entering 2026 with strong underlying support. Across all three Tier 1 contractors, the common themes were healthy revenue delivery, improving profitability, high backlog coverage and continued confidence in future tendering activity. While their business mixes differ, the combined message is clear: offshore investment remains resilient, projects are continuing to move through execution, and demand for subsea engineering, installation and offshore construction capacity remains firm.

What This Article Covers:

Reviews what the Q4 2025 results from Saipem, TechnipFMC and Subsea7 suggest about the health of the offshore market.

Highlights key takeaways on revenue performance, backlog strength and forward visibility across the Tier 1 contractors.

Explores what these results imply for the broader offshore sector in 2026, including market momentum and execution conditions.

Considers the likely impact on Tier 2 contractors, vessel owners and specialist service companies.

Briefly addresses how current geopolitical tensions could affect offshore activity, project delivery and market risk.

Concludes with what offshore players should be aware of as the sector enters 2026.

GRAPH 1: Quarterly Revenue Comparison

GRAPH 2: Full Year Revenue Comparison

S7 results point to a business that is executing steadily across conventional subsea work, while also strengthening its forward visibility. Group revenue rose to $7.1 billion in 2025, supported by strong O&G activity in Brazil, Norway and Türkiye, as well as some renewables markets.

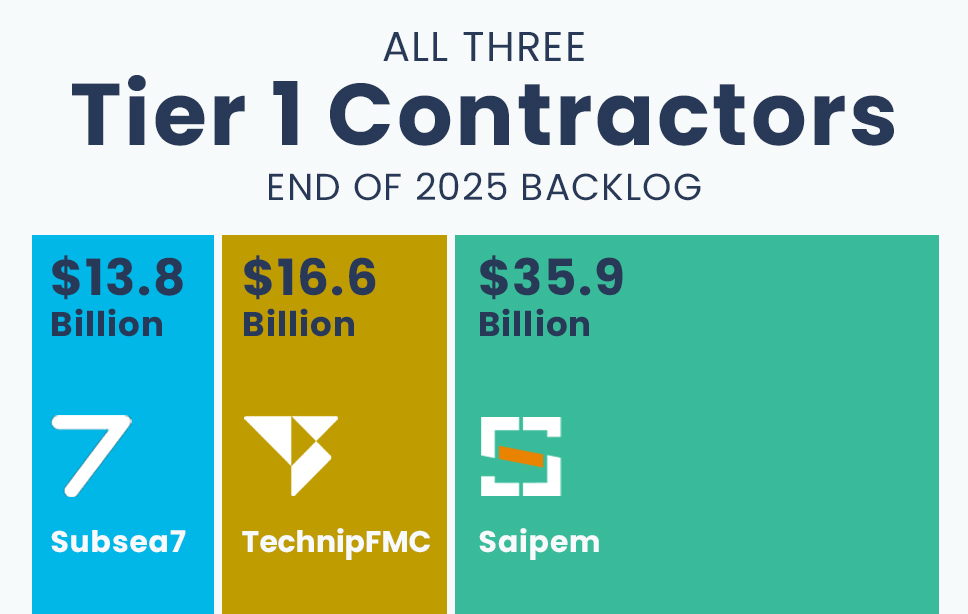

Just as importantly, S7 ended the year with a $13.8 billion backlog, backed by a 1.3x book-to-bill ratio and $9.0 billion of full-year order intake. Management emphasised that this backlog provides strong visibility into 2026 and beyond, with $6.9 billion already scheduled for execution in 2026 and backlog for 2027 up materially on the prior year. The broader message from Subsea7 is one of a contractor with balanced market exposure, healthy fleet demand and increasing confidence in utilisation into 2027, 2028 and beyond.

TFMC delivered the strongest full-year revenue growth of the three companies, with total company revenue rising to $9.9 billion in 2025. Although Q4 showed some moderation in subsea activity in regions such as the North Sea and Latin America, the full-year picture remained strong, particularly in Subsea, where the company continued to convert market demand into both growth and margin improvement.

The most important strategic takeaway is the strength of TFMC order position. The company ended 2025 with $16.6 billion of backlog, including $15.9 billion within Subsea, and highlighted that it has inbounded more than $30 billion of subsea orders over the last three years. Legacy projects now make up less than 10% of Subsea backlog, which points to improving backlog quality as well as scale. For the market, TFMC results reinforce the idea that the subsea cycle remains strong and that differentiated technology-led offerings are continuing to win work.

Saipem’s results highlight both the scale of its platform and the strength of current offshore construction markets. The company reported €15.5 billion of revenue in 2025, with Q4 described by management as its strongest quarter ever in terms of revenue, EBITDA and operating cash flow. Growth was led by Offshore E&C and Asset-Based Services, while Offshore Drilling remained softer due to fleet reductions, contract suspensions and relocation costs.

Backlog visibility remains one of Saipem’s clearest strengths. The company said that more than 90% of 2026 revenue is already covered by projects in backlog, while its construction vessels are fully booked for 2026 and utilisation for subsequent years is also building. Although Saipem’s business mix is broader than its more subsea-focused peers, the core takeaway is similar: the company enters 2026 with strong workload cover, high asset utilisation and good visibility on near-term offshore demand.

GRAPH 3: Backlog Comparison

Taken together, the results from the three Tier 1 contractors point to an offshore market that remains fundamentally healthy. Revenue growth suggests that offshore projects are continuing to move through execution, while large backlogs indicate that this is not just a short-term burst of activity. Indeed, the market has entered 2026 with a solid base of work already in hand.

The results also suggest that subsea and offshore construction remain among the strongest parts of the broader offshore value chain. In particular, the combination of high fleet utilisation, growing order books and improving margins indicates that demand is not only holding up, but doing so in a way that is commercially supportive for major contractors.

At the same time, the results also point to an important market characteristic for 2026: capacity and execution may matter as much as demand. Strong backlogs are positive, but they also imply tighter competition for vessels, equipment, engineering resources and offshore execution windows as more projects move into delivery.

For Tier 2 contractors, the Tier 1 results are broadly encouraging. When the largest offshore contractors are reporting strong backlogs, healthy order intake and high utilisation, it usually points to continued downstream demand for specialist subcontractors, equipment providers, survey firms, inspection providers, fabrication support, and other niche service companies.

However, the opportunity may not be evenly distributed. Tier 1 contractors with strong backlog positions are likely to remain selective in how they allocate work, and may prefer partners that can demonstrate reliability, technical differentiation, regional presence or proven delivery capability. In that sense, 2026 may be supportive for sector players, but it may also become more competitive and execution-focused.

For vessel owners, the implications are also constructive. High backlog levels and growing project execution should continue to support utilisation for subsea construction vessels, support vessels and other specialist offshore tonnage. At the same time, vessel owners may need to think carefully about fleet positioning, regional exposure and readiness, particularly in a market where timing, mobilisation and access to key basins are becoming increasingly important.

For the broader supply chain, the market appears supportive, but not easy. The strongest opportunities sit where specialist capability aligns with bottlenecks in execution, whether that is offshore installation support, vessel access, engineering capacity, inspection capability or other critical services tied directly to project delivery.

It is worth noting that the Tier 1 contractors published their latest quarterly results before February 28, 2026, the date Reuters identifies as the start of the current U.S.-Israeli war with Iran.

Geopolitics adds an important caveat to an otherwise positive market picture. The main risk is not a collapse in offshore demand, but a more difficult operating environment, with disruption around the Strait of Hormuz potentially increasing mobilisation risk, insurance costs and logistics complexity. At the same time, higher oil and gas prices and a renewed focus on energy security may continue to support offshore investment. In that sense, geopolitics may not weaken the offshore cycle, but it could make it more volatile and operationally complex.

Overall, the results suggest that offshore is entering 2026 from a position of strength. Demand remains healthy, backlog visibility is high, and the major contractors are showing continued confidence in project execution and future workload.

For the sector, the key issue is likely to be less about whether demand exists and more about how effectively companies can position themselves to capture it. Operators will need to keep a close eye on execution risk and contractor availability. Tier 1 and Tier 2 contractors will need to balance selectivity with delivery. Other vessel owners and service providers will need to think carefully about fleet deployment, basin exposure and the practical realities of supporting projects in a tighter and potentially more volatile market.

The overall message is positive, but not complacent: 2026 looks supportive for offshore activity, but success is likely to depend increasingly on capacity, positioning and execution resilience.

As more offshore projects move from award into execution, understanding contractor activity, vessel availability and regional market shifts becomes increasingly important. Through our offshore market intelligence and data solutions, EMA helps clients track project developments, monitor fleet activity and navigate a fast-moving global market with greater confidence.

From project tracking and contractor intelligence to vessel monitoring and regional market analysis, we help clients stay closer to offshore activity as it develops. Our insight supports earlier opportunity identification, stronger competitor awareness and better decision-making across an increasingly busy and complex offshore market.

📩 Get in touch with our Business Development Manager:

eric.sherman@energymaritimeassociates.com

Energy Maritime Associates (EMA) presented at the OSJ Subsea Conference in London on 2 February 2026. Our Executive Director, Michael Watson, spoke...

In a recent webinar hosted by Offshore Magazine and Energy Maritime Associates (EMA), David Boggs, Managing Director of EMA, examined the rapidly...

As the global oil and gas industry pivots towards floating production systems, Energy Maritime Associates (EMA) has released a pivotal report today...